Social Security’s trust fund is projected to be exhausted in 2034, only ten years from now. As a 64-year-old, this gets my attention! After the fund disappears, Social Security will still receive the funds from current year taxation of wages, an amount that the government predicts will cover about 80% of benefits.

Truxton’s older clients have income beyond Social Security (SS) benefits. But Social Security payments form a base. Budget and demographic issues will force some changes in the program over the next 25 years. The changes may affect affluent and wealthy recipients more than lower income seniors as Congress considers how to allocate the inevitable pain. One concept is “means testing”: determining benefit reductions based on the financial status of the beneficiary. This seems superficially “fair.” Surely poorer seniors cannot afford to see their Social Security reduced since they have little or no other income.

But Social Security and related programs are already “means tested” in several ways that are obscure to many current and potential program beneficiaries.

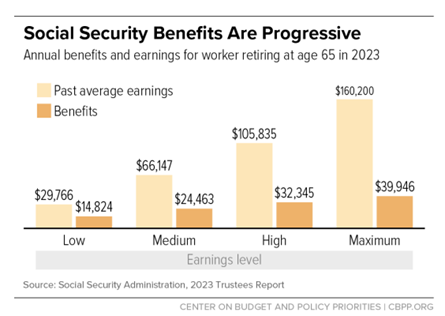

- Begin with the “Bend Points.” Almost no one knows the details of how Social Security benefits are calculated. The basics: The government records your Social Security taxed earnings over your lifetime. The benefit calculation depends on your earnings in your 35 inflation-indexed highest earning years. But not all earnings are assessed equally. The first $1,174 of average lifetime monthly earnings are multiplied by 90%, the next $5,905 by 32%, and income above this level (up to the Social Security taxable maximum) earn you 15%. So, people with consistent high income do receive more benefit than the “working poor” but far less, proportionally, than the greater tax that the affluent have paid. High earners can expect SS to replace 25% of their average lifetime income, while low earners will expect 50% or more to be replaced. This may be appropriate public policy, but it represents a high degree of effective means testing.

- SS benefits are taxable. Married taxpayers with an income above $44,000 will pay tax at their marginal rate on 85% of benefits, effectively clawing back 33% of the benefit for high income taxpayers. This dramatically increases the progressivity of Social Security benefits and amounts to yet another form of means testing.

- People who work for many years see no incremental benefit. Recall that SS only considers your 35 highest earning years. People with significant income from age 22 until age 65 will get no incremental benefit from the SS tax paid in eight of their working years. Those extra years of payments are a gift to the system. People who work well into old age are generous donors to people who work fewer years at lower pay. Wait by the mailbox for your thank you note.

- Couples with two high income earners are meaningfully penalized compared to one income couples. A one income couple receives 50% of the higher income spouses’ benefit, even if the other partner has had no earned income at all. The two-earner couple receives both spouses’ benefit but would have received half of that with only one income. Simply put, the two earner couple pays the full amount of both spouses SS tax, but only gets half of the marginal benefit, dramatically reducing the net return on the second spouses lifetime tax payments.

- Medicare is, of course, a separate program but is even more dramatically “progressive” in structure. A high-income taxpayer pays 2.9% (including employer payments) in Medicare tax, plus a supplemental tax of 1.8% on income above $200,000. A taxpayer with an income of $1 million is likely to pay over $40,000 in Medicare tax. Since 1992, this amount has been uncapped. A person with a $50,000 income pays $1450, 3% as much. With SS, at least the higher earner receives a greater benefit (though not proportionally so). With Medicare, the high earner receives exactly the same benefit as someone who has paid modest taxes. Highly progressive. A profound means test.

- Further, Medicare Part B premiums are sharply adjusted for income. Low income beneficiaries in 2023 pay $165 monthly, while very high income seniors pay as much as $560 a month, even though they have already paid far more in tax to receive identical benefits.

The Congress could decide to pay all earned benefits, supplementing the receipts from Social Security taxation from the general fund. But the Federal Government will experience a $2 trillion deficit this year at a moment of near record-low unemployment. Adding a large new obligation to the general fund would be imprudent and may be impossible.

If the government does decide to reduce benefits in the mid-2030’s, will they make “across-the-board” percentage reductions, cutting the benefits of the working poor by the same percentage as the relatively affluent? That seems unlikely. High income seniors receiving higher benefits are likely to feel higher pressure for cuts. Again, this may be appropriate public policy; the poor are far more vulnerable to reductions in benefits. But don’t let the pundits and the politicians tell you that they are introducing benefits means testing for the first time. Both of the major old age benefit programs are already highly progressive in their economic structure.

Social Security’s trust fund is projected to be exhausted in 2034, only ten years from now. As a 64-year-old, this gets my attention! After the fund disappears, Social Security will still receive the funds from current year taxation of wages, an amount that the government predicts will cover about 80% of benefits.

Truxton’s older clients have income beyond Social Security (SS) benefits. But Social Security payments form a base. Budget and demographic issues will force some changes in the program over the next 25 years. The changes may affect affluent and wealthy recipients more than lower income seniors as Congress considers how to allocate the inevitable pain. One concept is “means testing”: determining benefit reductions based on the financial status of the beneficiary. This seems superficially “fair.” Surely poorer seniors cannot afford to see their Social Security reduced since they have little or no other income.

But Social Security and related programs are already “means tested” in several ways that are obscure to many current and potential program beneficiaries.

The Congress could decide to pay all earned benefits, supplementing the receipts from Social Security taxation from the general fund. But the Federal Government will experience a $2 trillion deficit this year at a moment of near record-low unemployment. Adding a large new obligation to the general fund would be imprudent and may be impossible.

If the government does decide to reduce benefits in the mid-2030’s, will they make “across-the-board” percentage reductions, cutting the benefits of the working poor by the same percentage as the relatively affluent? That seems unlikely. High income seniors receiving higher benefits are likely to feel higher pressure for cuts. Again, this may be appropriate public policy; the poor are far more vulnerable to reductions in benefits. But don’t let the pundits and the politicians tell you that they are introducing benefits means testing for the first time. Both of the major old age benefit programs are already highly progressive in their economic structure.